Why Is My Mortgage Credit Score Lower Than What I See on Credit Karma?

Why Is My Mortgage Credit Score Lower Than What I See on Credit Karma?

A Local Guide for Homebuyers in Phoenix, Scottsdale, and Across Maricopa County

One of the most common questions I hear from homebuyers throughout Phoenix, Scottsdale, Mesa, Chandler, Gilbert, Glendale, Peoria, Surprise, Goodyear, Avondale, Tempe, Queen Creek, Anthem, Fountain Hills, and across Maricopa County is:

"Why did my mortgage lender pull a lower credit score than what I see on Credit Karma?"

If you're preparing to buy a home, you're not alone. Many Arizona homebuyers are surprised when they check their credit score online and see one number, only to have their mortgage lender pull a completely different score.

The good news is that this is normal.

The short answer is:

Credit Karma and many free credit monitoring services typically show a VantageScore, while most mortgage lenders use FICO® scores.

These are two different scoring models that often produce different results.

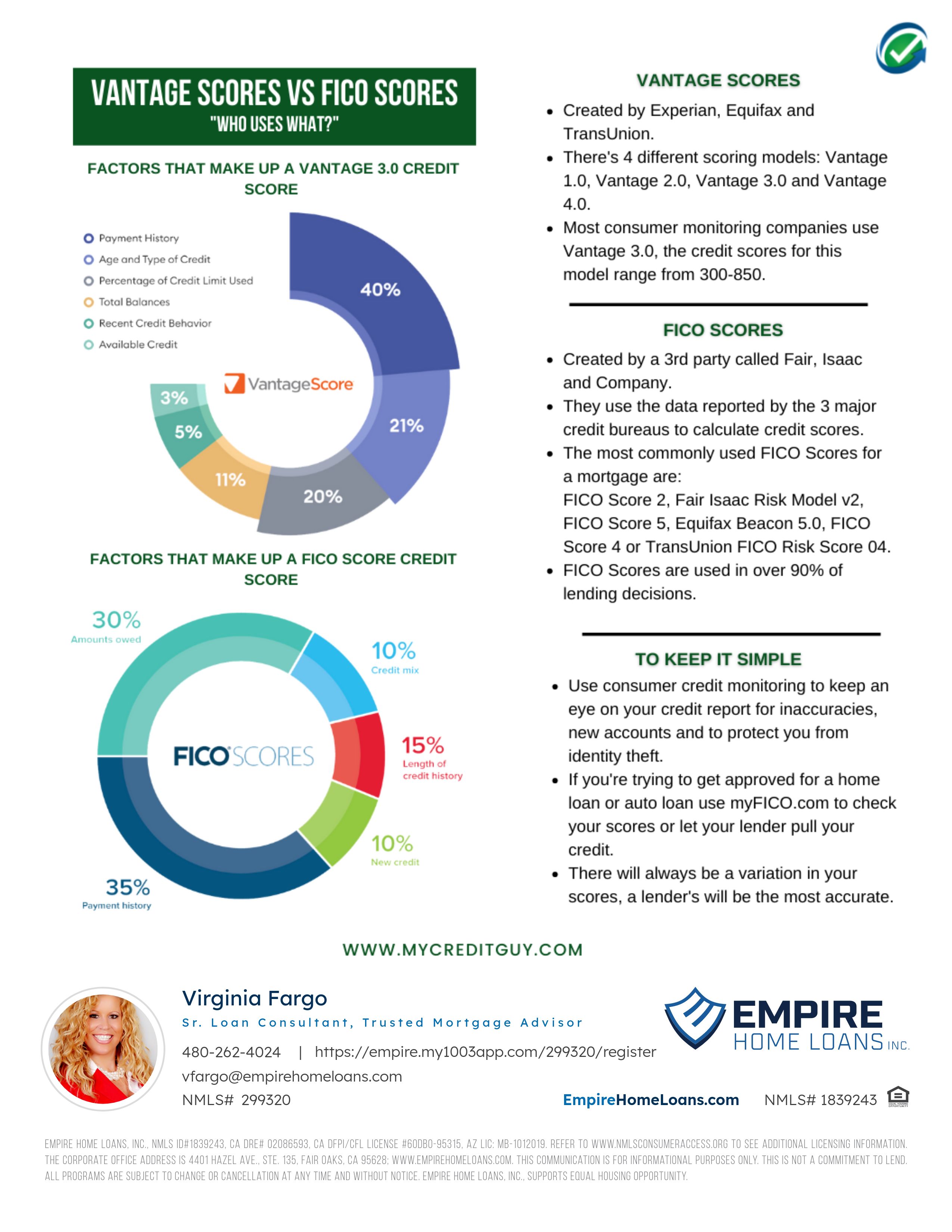

What Is a VantageScore?

VantageScore was created by the three major credit bureaus:

Experian

Equifax

TransUnion

Many popular credit monitoring websites and apps use VantageScore models, including:

Credit Karma

Credit Sesame

Many banking apps

Various free credit monitoring services

VantageScores generally range from 300 to 850 and are designed to help consumers monitor their credit health.

While these scores are useful for tracking trends, they are not always the scores used when applying for a mortgage.

What Credit Scores Do Mortgage Lenders Use?

Most mortgage lenders use mortgage-specific FICO® scores.

For many conventional, FHA, and VA loan programs, lenders typically review:

Experian FICO Score 2

Equifax Beacon Score 5.0

TransUnion FICO Score 4

Your lender generally uses the middle score of the three credit bureaus to determine qualification and pricing.

This is why your mortgage score may be significantly different from the score you see online.

Why Is My Mortgage Score Lower Than My Credit Karma Score?

Many homebuyers in Phoenix and Scottsdale are shocked when their mortgage score comes back lower than expected.

That's because mortgage FICO models place different weight on:

Payment history

Credit card utilization

Length of credit history

New credit accounts

Recent inquiries

Collection accounts

Overall debt management

Even though the information comes from the same credit bureaus, VantageScore and FICO use different formulas to calculate risk.

As a result, score differences of 20, 40, 60, or even 80 points are common.

Which Credit Score Matters When Buying a Home?

If you're applying for a mortgage in Phoenix, Scottsdale, or anywhere across Maricopa County, the score that matters most is the mortgage score pulled by your lender.

That score determines:

Whether you qualify

Which loan programs are available

Your interest rate

Your monthly payment

Mortgage insurance requirements

Your overall purchasing power

Your online score is useful for monitoring your credit, but your lender's mortgage score is what drives lending decisions.

Are Mortgage Lenders Starting to Use VantageScore?

Possibly.

The mortgage industry continues to evolve, and some lenders are beginning to explore VantageScore models.

However, most mortgage lenders today still primarily rely on FICO scoring models when underwriting FHA, VA, USDA, and conventional home loans.

What Factors Impact My Credit Score the Most?

According to FICO, the five major factors that influence your score are:

Payment History (35%)

Making payments on time is the single biggest factor affecting your score.

Amounts Owed (30%)

Credit card balances and utilization ratios have a major impact on mortgage scores.

Length of Credit History (15%)

Older, well-managed accounts typically help your score.

New Credit (10%)

Opening new accounts before applying for a mortgage can lower your score.

Credit Mix (10%)

A healthy mix of installment and revolving accounts can help strengthen your profile.

Common Mistakes That Hurt Mortgage Scores

Before applying for a mortgage in Arizona, avoid:

❌ Opening new credit cards

❌ Financing furniture or appliances

❌ Buying a new vehicle

❌ Missing payments

❌ Maxing out credit cards

❌ Co-signing for someone else's debt

❌ Paying balance down to $0.00 & Closing older credit card accounts

❌ Making large unexplained deposits or withdrawal

For many homebuyers in Phoenix, Scottsdale, and Maricopa County, paying down debt to 30% line of credit can:

Increase credit scores

Improve loan eligibility

Increase purchasing power

Potentially qualify for better interest rates

However, every situation is different.

Sometimes it's better to preserve cash for a down payment, closing costs, reserves, or emergency savings. Before paying off large amounts of debt, it's wise to consult with a mortgage professional to determine the strategy that best supports your homeownership goals.

How Can I Find Out My True Mortgage Credit Score?

The only way to know your mortgage score is to have a mortgage lender pull a mortgage credit report.

A mortgage credit report includes:

All three credit bureaus

Mortgage-specific FICO scores

Public records review

Detailed credit history analysis

This gives you the most accurate picture of where you stand before shopping for a home.

Frequently Asked Questions

Why is my Credit Karma score different from my mortgage score?

Credit Karma typically uses a VantageScore model, while most mortgage lenders use mortgage-specific FICO scores.

Which credit score do mortgage lenders use?

Most mortgage lenders use Experian FICO 2, Equifax Beacon 5.0, and TransUnion FICO 4.

How much can my scores differ?

Differences of 20 to 80 points are common.

Will checking my credit hurt my score?

A mortgage inquiry may cause a small temporary decrease, but mortgage shopping inquiries are generally grouped together and have limited impact when done within a designated timeframe.

Should I pay off my credit cards before applying for a mortgage?

no, do not pay credit cards or auto loans down to $0.00 balance, this will hurt your credit score.

Reducing card balances to 30% line of credit often improves mortgage scores and may increase purchasing power. However, every situation is different, so it's important to review your strategy before making major financial changes.

Is a 700 Credit Karma score the same as a 700 mortgage score?

Not necessarily. Mortgage scores can be higher or lower depending on the scoring models used and the information reported to the credit bureaus.

The Bottom Line

If you're planning to buy a home in Phoenix, Scottsdale, Mesa, Chandler, Gilbert, Glendale, Peoria, Surprise, Goodyear, Avondale, Tempe, Queen Creek, Anthem, Fountain Hills, or anywhere across Maricopa County, don't assume the score you see online is the same score your mortgage lender will use.

Understanding the difference between VantageScore and FICO scores can help you avoid surprises, improve your qualification strategy, and position yourself for the best financing options available.

Before you start house shopping, it's smart to know your true mortgage credit score and understand exactly where you stand.

Ready to Find Out Your Mortgage Credit Score?

A mortgage credit review can help determine:

Which loan programs you qualify for

Your estimated interest rate

Your purchasing power

Whether improvements could help you qualify for better financing terms

The fastest path to homeownership

Work With Us

We recognize that your needs are unique, and we would love to find out

exactly how we can be of service to you.

Contact us by email or give me a call.

CALL US

Call me today with any questions you have about the process - I'm happy to help.

CONNECT WITH US

Virginia Fargo

NMLS #299320

4401 Hazel Ave, Ste 135, Fair Oaks, CA 95628

Empire Home Loans NMLS #1839243

Facebook

LinkedIn

Instagram