What Is a Jumbo Loan in Maricopa County, Arizona? (2026 Guide for Self-Employed Homebuyers)

What Is a Jumbo Loan in Maricopa County, Arizona? (2026 Guide for Self-Employed Homebuyers)

Quick Answer: What Is a Jumbo Loan?

In Maricopa County, Arizona, a jumbo loan is typically any mortgage loan amount above $832,750 for a 1-unit property in 2026.

If your loan amount exceeds $832,750, the loan usually falls outside standard conforming loan limits set by Fannie Mae and Freddie Mac and becomes a jumbo mortgage loan.

This is especially common in Scottsdale, Paradise Valley, Arcadia, and other luxury areas across Maricopa County where home prices are often higher.

Last Updated: June 2026

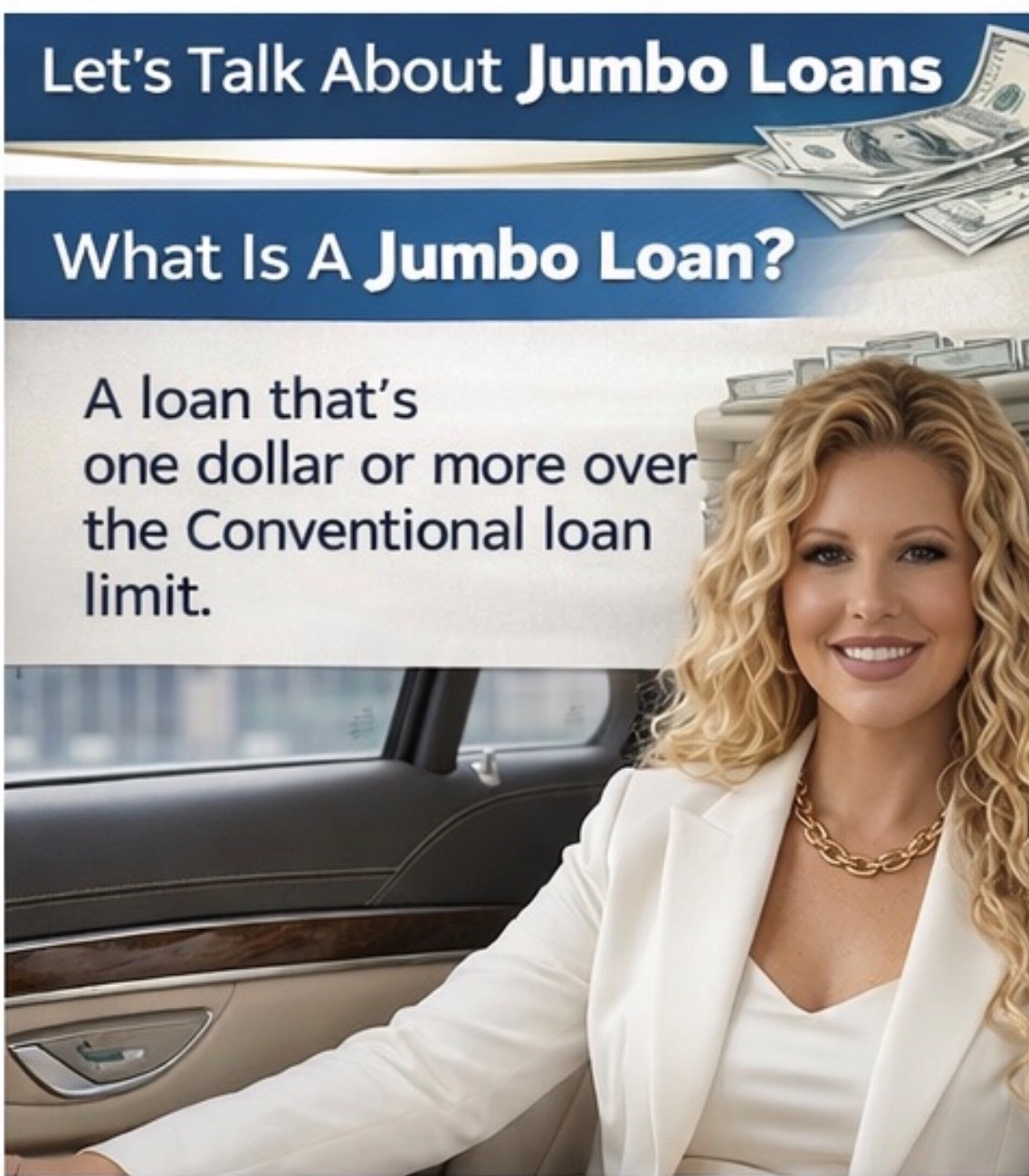

What Does “Jumbo Loan” Mean?

A jumbo loan is a home loan that exceeds the conforming loan limit for the county where the property is located.

For Maricopa County in 2026:

1-unit conforming loan limit: $832,750

Loan amounts above $832,750: typically jumbo loans

The loan limit applies to the loan amount, not the purchase price.

Scottsdale Jumbo Loan Example

Purchase Price: $1,050,000

Down Payment: $210,000 (20%)

Loan Amount: $840,000

Because the loan amount exceeds $832,750, this would generally be considered a jumbo loan in Maricopa County.

Why Jumbo Loans Matter in Scottsdale & Maricopa County

Many buyers relocating to Scottsdale are surprised by how quickly they cross into jumbo financing territory.

This is especially common with:

Luxury homes

Gated communities

Golf course properties

New construction homes

Larger homes with HOAs

North Scottsdale properties

Second homes and vacation properties

Even buyers putting substantial money down can still end up with a jumbo loan depending on the final loan amount.

Jumbo Loans for Self-Employed Borrowers

Many self-employed borrowers assume jumbo loans are impossible because traditional lenders may heavily scrutinize tax returns.

The reality is that many jumbo lenders offer alternative income documentation options for self-employed borrowers, business owners, entrepreneurs, independent contractors, and 1099 earners.

Depending on the program, qualifying income may potentially be calculated using:

Business bank statements

Personal bank statements

CPA-prepared P&L statements

Asset utilization

W-2 + bonus/commission income combinations

This can be especially helpful for Scottsdale entrepreneurs and business owners who write off significant business expenses on their tax returns.

Common Questions Self-Employed Jumbo Buyers Ask

How much down payment is required for a jumbo loan?

Down payment requirements vary based on:

Credit score

Occupancy type

Loan amount

Property type

Cash reserves

Income documentation

Some jumbo programs may allow lower down payment options than many buyers expect, while others require larger reserves and stronger financial profiles.

Are jumbo interest rates higher?

Not always.

In some market conditions, jumbo rates can actually be competitive with conforming loan pricing. Pricing depends on:

Market conditions

Credit profile

Assets

Documentation type

Loan structure

Fixed vs ARM options

Can self-employed borrowers qualify without tax returns?

Some jumbo programs may allow alternative income documentation options instead of full tax return qualification.

Program availability depends on the borrower’s overall financial profile and lender guidelines.

Is a jumbo loan harder to qualify for?

Jumbo underwriting is often more detailed than standard conforming financing.

Lenders may review:

Cash reserves

Business stability

Credit history

Debt-to-income ratios

Asset documentation

Income consistency

Preparing early can help create a smoother approval process.

Near the Jumbo Loan Limit? Here’s the Smart Strategy

If your estimated loan amount is close to $832,750, small adjustments may potentially help you remain within conforming loan limits.

Examples may include:

Increasing down payment slightly

Structuring seller concessions strategically

Reviewing property taxes and HOA costs early

Exploring different financing structures

In some cases, remaining conforming may reduce documentation requirements or improve financing flexibility.

In other cases, jumbo financing may actually be the better long-term option.

Work With a Local Scottsdale Mortgage Broker

Virginia Fargo #299320

Independent Mortgage Broker

Empire Home Loans #1839243

Serving Scottsdale, Phoenix & Maricopa County

Specialties include:

Self-employed borrowers

Jumbo mortgage financing

Relocation buyers

Bank statement loans

Business owner financing strategies

First-time luxury homebuyers

If you are unsure whether your loan amount falls into jumbo financing territory, Virginia Fargo can help review your scenario and compare potential conforming vs jumbo loan strategies based on your goals and financial profile.

Frequently Asked Questions

Does the jumbo loan limit change by city?

No. Loan limits are generally set at the county level, so Scottsdale, Phoenix, Tempe, Chandler, and other Maricopa County cities follow the same conforming loan limit.

What counts toward the jumbo loan limit?

The loan amount determines whether financing is conforming or jumbo — not the purchase price.

What if my loan amount is exactly $832,750?

Generally, loan amounts at or below the conforming limit are considered conforming, assuming the loan otherwise meets agency guidelines.

Are condo jumbo loans different?

Sometimes. Condo financing can involve additional review requirements depending on the project, HOA, occupancy levels, reserves, and lender guidelines.

This can be important in Scottsdale luxury condo communities.

Can I close a jumbo loan remotely if I’m relocating?

In many cases, yes. Remote and hybrid closing options may be available depending on title company procedures, lender requirements, and state regulations.

Important Disclosure

This information is intended for educational purposes only and should not be considered a commitment to lend. Loan approval is subject to credit approval, income verification, property approval, and underwriting guidelines. Program availability and loan limits may change without notice.

Work With Us

We recognize that your needs are unique, and we would love to find out

exactly how we can be of service to you.

Contact us by email or give me a call.

CALL US

Call me today with any questions you have about the process - I'm happy to help.

CONNECT WITH US

Virginia Fargo

NMLS #299320

4401 Hazel Ave, Ste 135, Fair Oaks, CA 95628

Empire Home Loans NMLS #1839243

Facebook

LinkedIn

Instagram